Don’t get caught offside by HMRC: Self-employed guide to apportioning business and leisure costs if heading to the 2026 World Cup

Wondering if you can write off your flights to the 2026 World Cup as a business expense if you are on a working holiday? Here is how to apportion travel expenses when self-employed so you can stay onside with HMRC and still enjoy the football

If you are jetting off to Mexico, Canada, or the United States this summer because you’ve suddenly developed a burning desire to network with target clients in Toronto, New York, or Miami, that is one thing.

However, if the truth is that the World Cup is calling and you are crossing the Atlantic to see if football is finally coming home, you must be careful what you claim during your working holiday. As a solo self-employed worker or small business owner trying to mix business with pleasure, every single purchase will leave a voice in your head whispering: “Can I write this off?”

HMRC’s infamous “wholly and exclusively” rule usually acts as a party pooper for mixed-use trips. If the taxman smells “dual purpose” whereby you planned a holiday and sprinkled a bit of work on top, he will gleefully disallow your entire flight cost.

However, if you play by the rules and learn how to apportion travel expenses when self-employed, you can legally claim for the business portions of your trip.

Here is how to referee your own tax return without getting a red card.

Separating business from personal travel expenses

HMRC’s Business Income Manual states that if an expense can be broken down into identifiable chunks, you can claim the specific part that belongs to your trade. Think of it as being split into distinct halves like a football match.

If you spend four days in Los Angeles pitching to a client and then catch a flight to Miami for a group-stage match, you cannot bundle it all together into one big “business trip” invoice. You must isolate the costs.

Total trip costs

──► Business Days (Hotel, Food, Local Taxis) ──► 100% Deductible

──► Match Days (Stadium Travel, Match Tickets) ──► 0% Deductible (Personal)

How to make an apportionment match strategy

To satisfy an auditor, your maths do not need to end up in the penalty box. Let’s look at how to break down the two most contentious costs: accommodation and those expensive transatlantic flights.

Per-night apportionment (accommodation & food)

This is the straightforward part. You look at your itinerary and count the days spent doing actual, billable work or active business development.

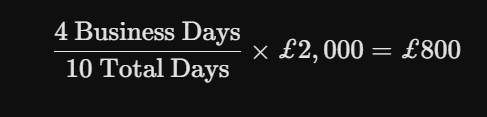

Here’s a scenario, for example. You book a 10-night stay in the US. For 4 days, you are attending a trade conference or holding face-to-face client meetings. The other 6 days are spent wearing face paint in a stadium.

Now, if your total hotel bill is £2,000, your allowable business expense is strictly calculated by the business ratio:

You can claim the £800. The remaining £1,200 is funded by your own personal entertainment budget. The same strict ratio applies to your daily meals (subsistence). Each time you make a trip to the concessions stand, you’ll be thinking you have just paid the equivalent of a round-trip flight from London to Barcelona with just a few beers and some nachos (and you can’t claim it on business expenses).

Of course, if you are a freelance sports reporter or travel and lifesytle journalist, you might be able to cover some of the costs of the matches, flights, hotel and food. But for most people, the cost of the sports events but be directly linked to your business. Call your accountant if you have any doubts before cliaming.

Flight conundrum: what can you expense?

This is where most self-employed people accidentally score an own goal, so consider it the ultimate VAR review. If you bought your flights specifically because you wanted to go to the World Cup, the flight has a dual purpose from day one. In that case, HMRC will completely disallow the flight cost. Also, did you tick the box for a business or leisure trip on your ESTA application? Or a mix of both?

However, if the primary, non-negotiable catalyst for the trip was a genuine business contract that required your physical presence in the US, and you merely decided to stay on for the football afterwards, the personal element is deemed incidental.

Here’s an HMRC tip to keep in mind. If the business trip came first, you can claim the full cost of the outbound and return flights. But if you extended the trip for the football, any extra internal flights between host cities (e.g., flying from your client in New York to a match in Texas) are strictly personal and cannot be claimed.

Keep a paper trail that puts VAR to shame

If HMRC decides to audit your return, they won’t just take your word for it. You need proof that you actually worked. To successfully apportion travel expenses when self-employed, ensure you have:

A pre-dated paper trail: Emails, contracts or event tickets showing the business meetings were arranged before you started booking stadium seats.

Daily business diary: Log exactly what business activity you did each day. “Answered three emails while waiting for the kickoff” does not count as a business day. “Four-hour strategy consultation with X Corp” does.

Split invoices: Where possible, ask hotels for itemised bills or book your business accommodation separately from your holiday accommodation.

By keeping your calculations transparent and your documentation organised, you can enjoy the football knowing that your tax return is as perfectly executed as a top-corner free kick (sorry, we couldn’t help ourselves).